India Stack: Inverting the Innovation Pyramid

On the occasion of World IP Day, let us take a look at the progress and continuous improvement in India Stack and how it promises to accelerate innovation across the fold.

On the occasion of World IP Day, let us take a look at the progress and continuous improvement in India Stack and how it promises to accelerate innovation across the fold.

India Stack is the moniker for a set of open APIs and digital public goods that aim to unlock the economic primitives of identity, data, and payments at population scale for a variety of services to customers through digital means.

India Stack consists of three layers: the identity layer, which serves as both a tool for identification and a facilitator of authentication, using Aadhaar and other digital authentication tools. The payment layer offers digital payment options like UPI and e-wallets for fast and seamless transactions. The data layer includes digital records and data that can be securely shared across different entities.

India Stack's open APIs enable developers to create innovative digital solutions for various use cases, such as identity verification, payments, and e-signatures. It is a government-backed initiative that aims to make India a cashless and paperless economy, accelerating digital transactions in the country.

India Stack has revolutionised the delivery of digital services in India, making them more accessible and inclusive. It has been adopted by banks, fintech companies, and government agencies, promoting financial inclusion and digital entrepreneurship. One successful example of India Stack is the Unified Payments Interface (UPI), which enabled over 8 billion transactions worth over 237 billion USD in January 2022 alone, according to the National Payments Corporation of India (NPCI).

While India Stack was fundamentally created to benefit the citizens of India, the country, which runs on the ideals of Vasudhaiva Kutumbakam (the world is one family), never hesitated to share the technology with her global brethren. The fundamental vision driving India Stack is the creation of open networks that provide a level playing field for members of a digital ecosystem. This enables application developers to concentrate on building the best consumer experiences and products, without having to worry about infrastructure, permissions, or access. None of the systems within India Stack relies on proprietary technology or intellectual property, making them implementable in other countries as well.

India Stack: Building a robust innovation platform

Currently, there are two open network implementations within India Stack. The first is the Open Credit Enablement Network (OCEN), which facilitates easy transmission of credit to consumers and businesses. The second is the National Digital Health Mission, an open network that enables consumers to securely share their health data with a network of healthcare apps and providers.

Many countries have applauded India Stack's success and expressed interest in acquiring the system. The Modular Open Source Identity Platform (MOSIP) is an open-source foundational identity platform developed by the International Institute of Information Technology in Bengaluru on which national foundation IDs are built. It has partnered with Sierra Leone's National Civil Registration Authority to create a digital ID pilot project similar to India's Aadhaar. India's success in developing Aadhaar and a range of open APIs known as India Stack has inspired a global digital revolution. MOSIP has already partnered with 11 countries, with five rolling out nationwide programmes and six evaluating large pilot programmes. Sri Lanka, Morocco, the Philippines, Guinea, Ethiopia, and the Togolese Republic are among the countries already using MOSIP. Tunisia, Samoa, Uganda, and Nigeria have expressed interest in adopting the Indian model.

As of September 2022, 100% of the adult population in India has an Aadhaar and even between 2-18 years of age, it’s above 80%. This massive enrolment allows for seamless digital identity verification, making transactions and services accessible to more people. Nearly 1,200 government schemes and programs, run by both the central and state governments, are using Aadhaar-based identification for the delivery of services.

A recent report by PhonePe and Boston Consulting Group has concluded that India's digital payments market is expected to more than triple from $3 trillion to $10 trillion by 2026. Digital payment transactions have significantly increased as a result of the coordinated efforts of the government, along with other stakeholders, from 2,071 crore transactions in FY 2017-18 to 8,840 crore transactions in FY 2021-22.

India Stack also includes the Unified Payments Interface (UPI), which recorded 8.7 billion transactions in March 2023 alone, marking an 82% increase in usage in the financial year 2022-23 compared to the previous year. Around 200 banks and payment service providers in India offer UPI-based payment services, making it the most widely used payment system in the country.DigiLocker, the country's first secured cloud-based platform for storage, issuance, and verification of documents and certificates in a digital manner, has crossed 100 million users. Led by Aadhaar card details, the app has issued around 4.94 billion documents so far and currently has 101.1 million registered users. DigiLocker enables Indians to digitally store a copy of 568 various documents on a secure Cloud platform.Over 4 crore digital health records of individuals have been linked to the Ayushman Bharat Health Account (ABHA) accounts under Ayushman Bharat Digital Mission (ABDM), the backbone of India’s digital health system. This digital infrastructure has greatly improved the accessibility and efficiency of healthcare services in India.Over the past two decades, India has built the world's largest digital payments infrastructure, with digital transactions accounting for about 20% of the country's GDP. By 2025, digital transactions are expected to account for 71% of all transactions, with 800 million unique mobile payment users. However, the country cannot achieve true financial inclusion without integrating its 60 million micro, small, and medium enterprises (MSMEs) into the digital payments infrastructure. Unfortunately, 95% of Indian MSMEs lack access to financial services.To address this, the financial services industry in India needs to expand awareness and merchant acceptance of digital payments for MSMEs. This can be achieved by mapping the complex interconnections within each industry's networks, launching sector-specific embedded payment solutions, reimagining outdated business models, developing interoperable vendor and distribution systems, and conducting focused education and awareness campaigns.The India Stack has successfully established a robust digital economy by implementing a foundational approach that involves public infrastructure and policies. The use of a digital ID system and common APIs has stimulated innovation and choice for consumers. Interoperability has encouraged competition in digital financial services within the India Stack ecosystem, and data fiduciaries have enabled greater user control over individual data, leading to an open-data economy that spans multiple sectors.OCEN, launched in July 2020, is expected to bring greater transparency, efficiency, and competition to the Indian credit market by enabling more players to participate and leverage data-driven insights to make better lending decisions. The framework is still in its early stages of adoption, but it has the potential to revolutionise the Indian credit market and improve financial inclusion for millions of people. By delivering financial products directly to MSMEs, OCEN aims to reduce their dependence on traditional lenders and empower them. Unlike the traditional lending approach of the “lend and forget" ideology, digital lending is based on a "lend, monitor, and collect" approach.OCEN leverages the Account Aggregator (AA) system to revolutionise digital lending. AA is a regulated entity by the Reserve Bank of India (RBI) that enables secure and digital access to an individual's financial information held in one institution and shares it with any other regulated financial institution in the AA network. However, data sharing requires the individual's consent.In May 2022, the government launched the Open Network for Digital Commerce (ONDC) to complement this initiative. ONDC aims to establish open networks for exchanging goods and services in e-commerce, making it more accessible and inclusive for consumers by providing them with a range of local businesses to choose from. Currently, ONDC is being piloted in various cities across India and has facilitated 4000 successful transactions, creating a level playing field in the e-commerce sector dominated by industry giants like Amazon and Flipkart. ONDC's promotion of digitisation of small businesses and fostering of equal opportunities for MSMEs is driving the economic growth and development of the country.In addition to ONDC, the government launched the Open Credit Enablement Network (OCEN) to provide timely and affordable capital to small businesses. Together, ONDC and OCEN create a more inclusive and vibrant digital commerce ecosystem in India.

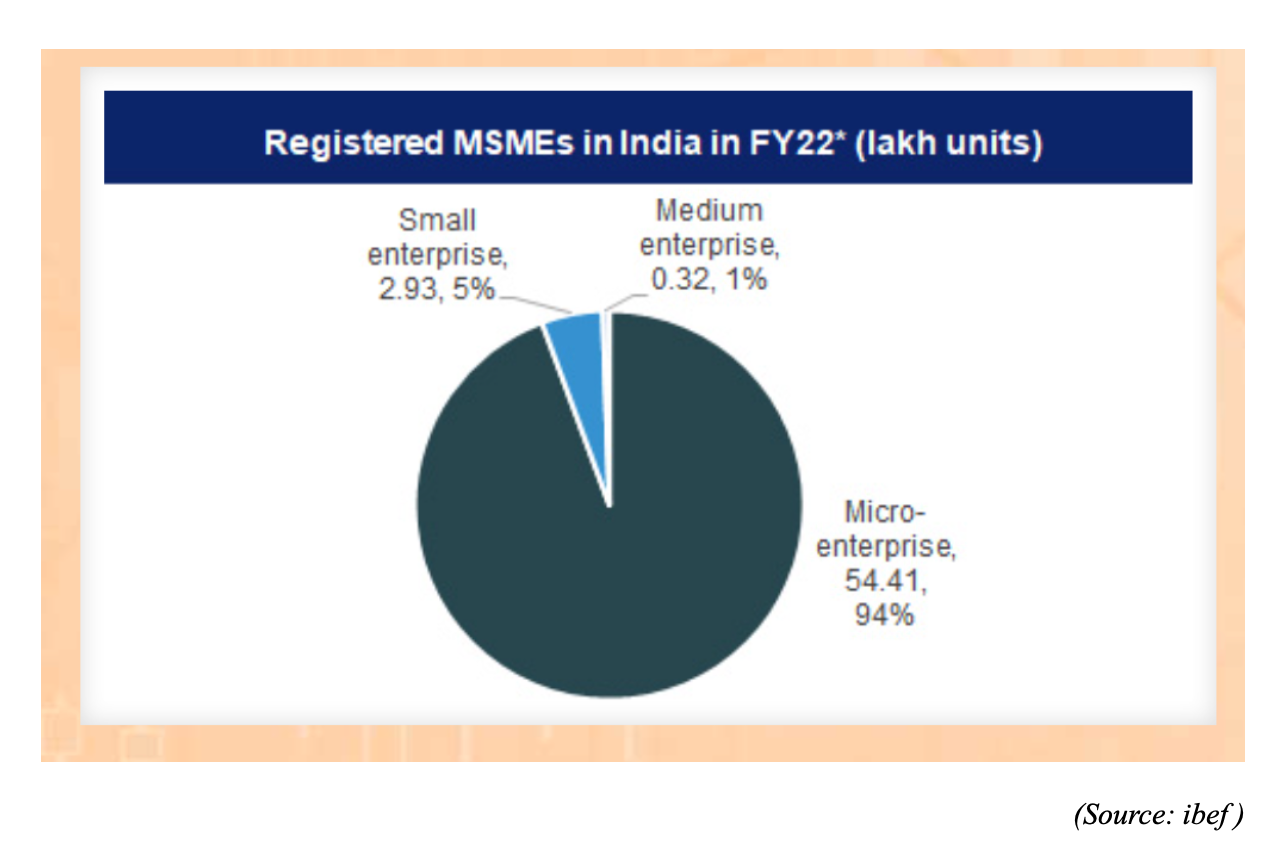

When MSMEs adopt digital payments, lenders can derive in-depth data insights related to their cash flow, working capital, inventory, markets, entrepreneur identification, and skills. This will help bridge India's MSME credit gap of $380 billion and lead to social upliftment for the 110 million low-socioeconomic people employed by these MSMEs. The MSME sector comprises nearly 63 million enterprises, which contribute 30 per cent to India's GDP, 45 per cent to manufacturing, 40 per cent to exports, and provide employment to over 113 million people, according to government data.

India Stack has transformed the way women entrepreneurs operate in India. With its digital identity infrastructure, women entrepreneurs can now easily access government services and financial institutions. Thanks to its payment infrastructure, accepting digital payments has never been easier, making transactions faster and more efficient. India Stack's digital lending platforms have also been a game-changer for small business owners, especially those in rural areas who struggle to access credit.

But that's not all. India Stack's digital marketplaces have given women entrepreneurs a platform to sell their products and services online, reaching a broader audience than ever before. Additionally, the eKYC and Aadhaar-based e-signature systems have streamlined the business registration process, making it faster and more straightforward for women entrepreneurs to start their own businesses.

According to YourStory Research Data, 214 fintech and financial services, startups have been established by women founders or co-founders in India over the past 12 years. Additionally, 18% of registered MSMEs in the UDYAM portal are owned by women. Nasscom and Zinnov report that 18% of startups in India are led by at least one woman founder or co-founder, and in 2022, almost $4.3 billion worth of capital flowed into women-led startups. India has more than 2,200 funded women-led startups.

When women are given the right tools and resources to succeed, their businesses can thrive. India Stack has created an ecosystem designed to remove barriers and provide women entrepreneurs with the support they need to succeed in the digital age. By simplifying access to capital, creating business models that leverage their existing skills and resources, providing safe working spaces, and fostering peer-to-peer communities, IndiaStack is empowering women entrepreneurs to achieve their business goals. Through these initiatives, IndiaStack is not only boosting the growth of women-owned businesses but also contributing to the overall development of the Indian economy.

India is on track to surpass Japan and Germany and become the world's third-largest economy by 2027, aided by its investments in technology and energy, as well as global trends. A decade ago, India began its push towards digital economy with the creation of Aadhaar. As India's economy grows, India may see an increase in disposable income. India's income distribution is forecast to shift significantly, with overall consumption potentially doubling from $2 trillion in 2022 to $4.9 trillion by the end of the decade. Non-grocery retail, including apparel and accessories, leisure and recreation, and household goods and services, among other categories, are expected to benefit the most. Credit availability is a crucial component of economic growth, and India currently has one of the lowest ratios of credit to GDP in the world. This is believed to increase from 57% to 100% over the next decade.To ensure fair competition in the industry, a level playing field for data flows is necessary. As the India Stack expands into processing insurance and health data, non-traditional data will become increasingly critical. The India Stack's approach can foster open finance, creating synergies across banking, wealth management, insurance, and other products globally

On the occasion of World IP Day we would like to invite you to be a part of it by joining this link.

Written by: Shivani; Edited by: Aurko; Visualisations by: Raghav